Social Security May Run Out by 2033: How to Create Bulletproof Backup Income in Under 10 Minutes

- Daniel Clink

- Dec 11, 2025

- 5 min read

If you're like most Americans, you've been counting on Social Security to be there when you retire. Here's the wake-up call nobody wants to hear: it might not be.

The Social Security Administration's own projections show the Old-Age and Survivors Insurance Trust Fund will be depleted by 2033. That's less than eight years away. And if recent legislation is any indicator, that timeline just got shorter. The "One Big Beautiful Bill Act" signed in July 2025 has already pushed the depletion date up to 2032.

We're not here to sugarcoat the situation or sell you false hope. We're here to tell you the truth and show you exactly how to protect yourself and your family before it's too late.

What "Depletion" Really Means for Your Retirement

Let's cut through the political noise and focus on the numbers that matter to your family's future.

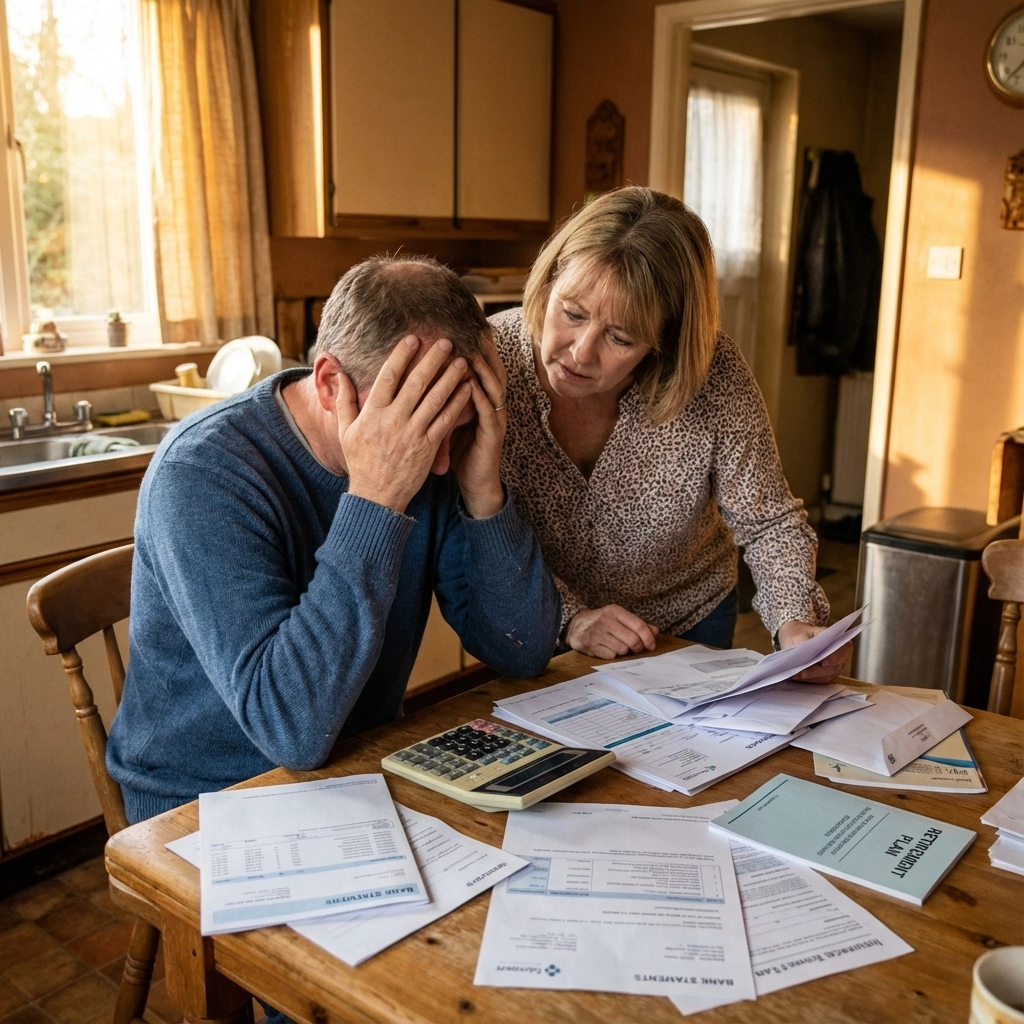

When the Social Security Trust Fund runs dry, it doesn't mean Social Security disappears overnight. But here's what it does mean: you'll face an immediate 23% cut in your expected benefits.

Think about that for a moment. If you're expecting $2,000 per month from Social Security, you'd suddenly be looking at $1,540 instead. That's $460 less every single month – $5,520 less per year. Over a 20-year retirement, that's more than $110,000 in lost income.

For millions of Americans who rely on Social Security as their primary retirement income source, this isn't just a financial setback – it's potentially devastating.

The Math That Should Keep You Up at Night

We're not typical insurance agents who paint doom and gloom scenarios to sell policies. We deal in facts. And the facts are sobering.

The average American retires with about $152,000 in retirement savings. Social Security benefits average around $1,900 per month. For most people, that Social Security check represents 40-60% of their retirement income.

Now imagine losing 23% of that overnight.

Even if Congress acts to prevent the worst-case scenario, any solution will likely involve some combination of benefit cuts, tax increases, or raising the retirement age. None of these options put more money in your pocket.

The harsh reality? You cannot count on Social Security to maintain its current benefit levels. Your retirement security depends on what you do right now to build alternative income streams.

The 10-Minute Solution: Building Bulletproof Backup Income

Here's where we do things differently. While other financial advisors might recommend complex investment strategies or tell you to "just save more," we focus on guaranteed solutions that work regardless of market conditions.

You can start building bulletproof backup income in the time it takes to drink your morning coffee. Here's how:

Step 1: Assess Your Income Gap (2 minutes)

Take your expected Social Security benefit and multiply it by 0.77 (that's what you'll actually receive after the 23% cut). Subtract that number from your expected full benefit. That's your annual income gap.

For example:

Expected annual Social Security: $24,000

After 23% reduction: $18,480

Annual income gap: $5,520

Step 2: Calculate Your Backup Income Need (3 minutes)

Your backup income sources need to fill that gap and provide additional security. We recommend planning for 150% of your gap to account for inflation and unexpected expenses.

Using our example: $5,520 × 1.5 = $8,280 per year needed from backup sources.

Step 3: Choose Your Guaranteed Income Strategy (5 minutes)

This is where smart families separate themselves from the crowd. While traditional investments rise and fall with market volatility, insurance-based income strategies provide guarantees when you need them most.

Fixed Annuities: Lock in guaranteed income rates now while they're still attractive. A $100,000 fixed annuity can generate $500-600 per month for life, regardless of what happens to Social Security or the stock market.

Whole Life Insurance with Cash Value: Build tax-advantaged wealth that grows regardless of market conditions. Many of our clients use these policies as personal pension plans, accessing cash value through loans during retirement.

Indexed Universal Life (IUL): Capture market upside with downside protection. Your cash value grows with market gains but never decreases due to market losses.

Why Insurance-Based Income Beats Traditional Retirement Planning

We're going to be direct: traditional retirement advice is failing American families. The "4% withdrawal rule" assumes your investments will always be there. Market-based strategies leave you vulnerable to sequence of returns risk – the possibility that poor market performance early in retirement destroys your financial security.

Insurance-based income strategies provide what traditional investments cannot: mathematical guarantees.

When you work with The Lions Den Insurance Group, you're not just buying a policy – you're building a fortress around your family's financial future. Our strategies work whether the stock market soars, crashes, or Social Security benefits get cut in half.

Real-World Example: The Johnson Family's Backup Plan

Let me tell you about Sarah and Mike Johnson (names changed for privacy). Both teachers, they realized their pensions plus Social Security wouldn't be enough, especially with the looming benefit cuts.

Here's what they did:

Purchased a $150,000 fixed annuity that guarantees $750 monthly income starting at age 65

Opened a whole life policy with $300 monthly premiums that builds cash value they can access tax-free

Set up an IUL policy for their 35-year-old son to ensure generational wealth transfer

Total monthly commitment: $650 Guaranteed monthly retirement income from these strategies alone: $1,200+

That's $14,400 per year in backup income – nearly triple what they need to replace their projected Social Security shortfall.

The Time Factor: Why Tomorrow Starts Today

Here's the uncomfortable truth: every month you wait makes this harder and more expensive.

A 45-year-old can build significant backup income with relatively modest monthly commitments. A 55-year-old faces much higher costs for the same results. A 65-year-old has extremely limited options.

The power of guaranteed growth and compound interest works best over time. Start now, and your small monthly commitments can create substantial income streams. Wait until you're closer to retirement, and you'll need massive lump sums to achieve the same results.

Your Next Steps: From Worry to Security

We've shown you the problem and given you the solution. Now it's time for action.

Step 1: Book a consultation with our team. We'll analyze your specific situation and show you exactly how much backup income you need.

Step 2: Review your current retirement accounts and Social Security projections. Many people discover their shortfall is larger than they realized.

Step 3: Choose the guaranteed income strategy that fits your timeline and budget. We'll design a custom plan that ensures you never depend on politicians to determine your retirement security.

The families who thrive in retirement don't hope for the best – they plan for the worst and build systems that work regardless of external circumstances.

Your legacy starts now. Your financial security doesn't have to depend on Social Security's uncertain future.

At The Lions Den Insurance Group, we empower families to build bulletproof financial protection that withstands any storm. We're not typical agents selling generic policies. We're your partners in creating guaranteed income streams that provide security when everything else fails.

The Social Security crisis is real. Your response to it will determine whether you retire with dignity or spend your golden years worried about money.

Let's build your backup plan today.

Comments